Two major rate decisions are in focus this week. The first comes from the United States on Wednesday, where the FOMC is expected to keep the fed funds rate steady within the 4.25%–4.50% range. The last time the Fed cut rates was in December last year, reducing by 25bps. Since then, Trump’s term, combined with tariff-driven inflation pressures, has limited Jerome Powell’s room to ease policy further.

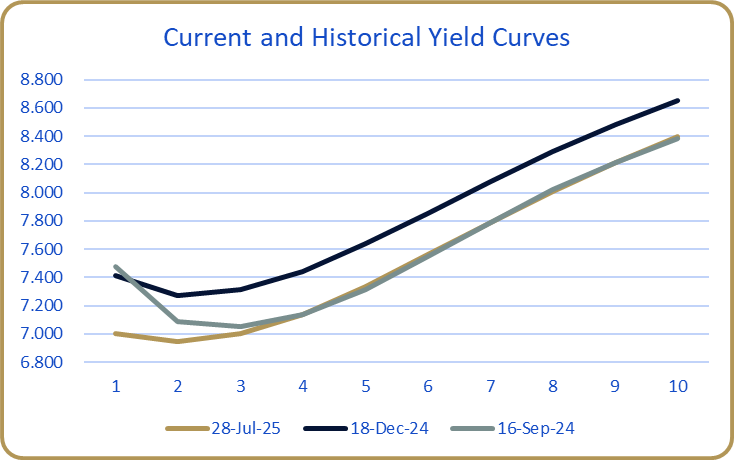

On Thursday, attention shifts to the SARB, which will deliver its latest interest rate decision. The front-end of the curve remains anchored, with the 1×4 FRA trading at 7.10% and the 1-year swap at 7.00%. The market is currently expecting a 25bps cut, which would bring the repo rate down from 7.25% to 7.00%. Finally, on Friday, the Eurozone is set to release its latest inflation figures. The Core CPI (YoY) is expected to remain unchanged at 2.3%.