After last week’s flurry of economic activity, this week is notably quieter with no major announcements on the calendar. This offers an opportunity to reflect on recent developments and the current interest rate landscape.

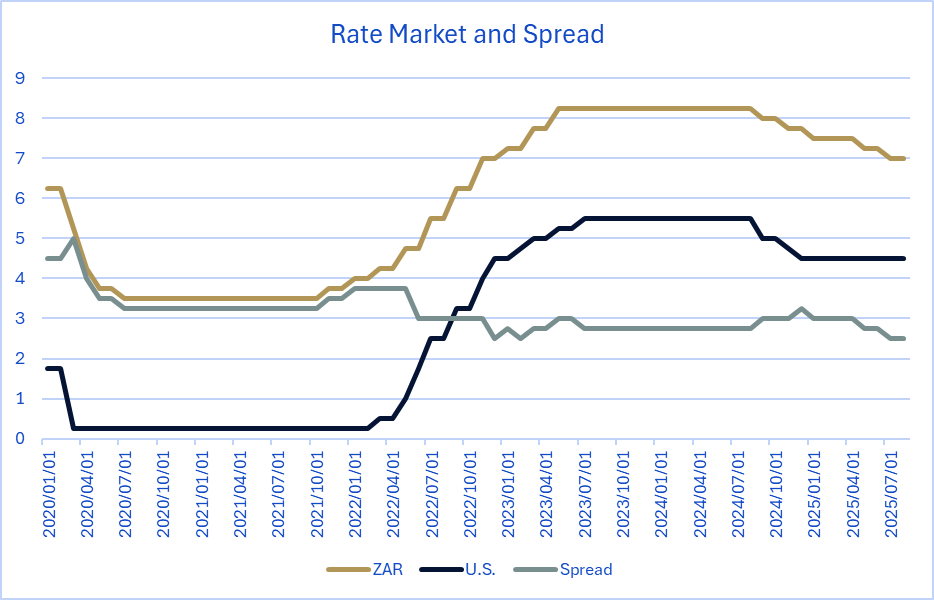

The FOMC cut rates for the first time since December last year by 25bps, a move that provides room for the SARB to consider easing in future meetings. Prior to this cut, the spread between the Fed Funds rate and the Repo rate had narrowed to just 2.5%, its smallest level in five years.

Graph 1: Repo and FED rate spread

Domestically, the MPC held rates steady at 7.00% with a 4 to 2 vote split between holding and cutting. The decision has supported ZAR strength, with the currency firming to 17.34 against the USD. Similar gains have been seen against other major currencies, with EUR at 20.36 down from 20.58 last week and GBP at 23.36 down from 23.70.

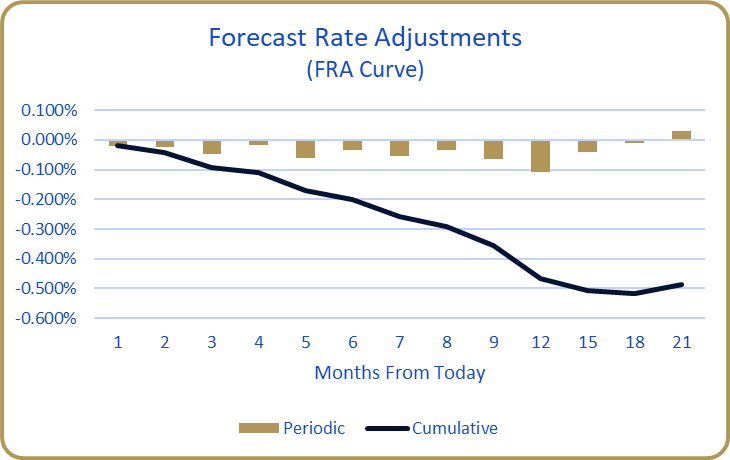

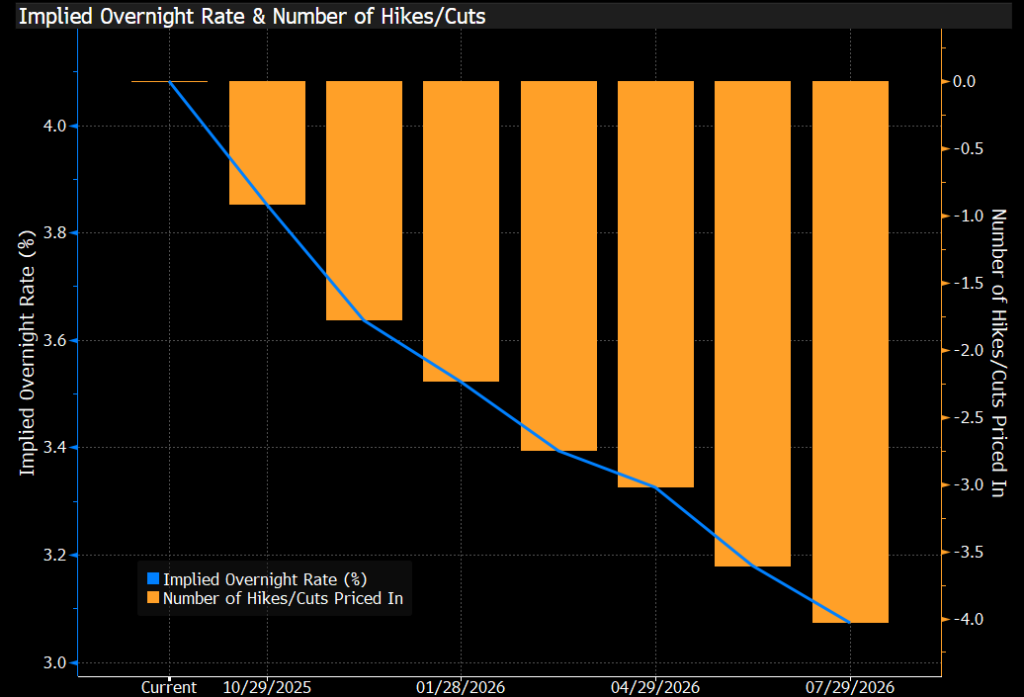

Looking ahead, the US market is pricing in just under two additional cuts before year end, while the South African curve remains far more cautious, with only around 10bps of easing expected.

Graph 2: Bloomberg US WIRP snapshot

Graph 3: ZAR FRA curve