Market conditions for Hedging Interest Rates and Foreign Exchange

With the interest rate cycle appearing to top out locally and globally the impression can be that no hedging is required, or that hedging may be expensive. This is not necessarily the case. On Friday 25 August, Jerome Powell stuck to the FED’s hawkish rhetoric and committed to the 2% inflation target.

The following slides will cover:

- The historic movement of interest rates and foreign exchange;

- Some of the key factors that drive these markets;

- The potential future range of interest rates and foreign exchange rates based on our proprietary Monte-Carlo simulation models for these domestic exposures;

- The current cost of hedging in the markets; and

- How much hedging is necessary (for each company to determine, based on their risk appetite).

Bastion provides this service to its clients i.e., assisting with such an evaluation.

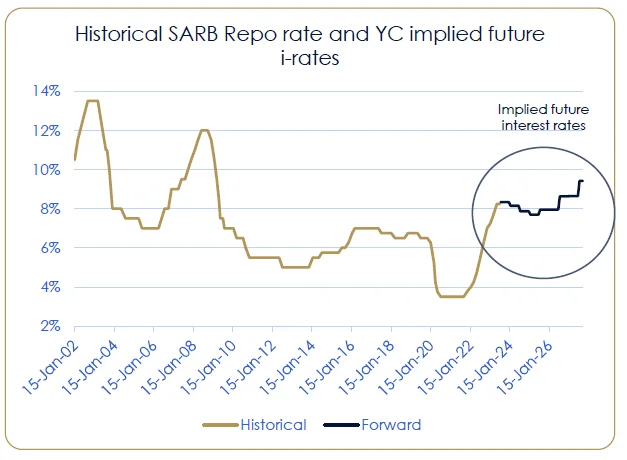

Where is RSA in the interest rate cycle?

- The SARB MPC kept the Repo rate unchanged at 8.25% at the last meeting (next meeting is 21st Sept 2023)

- RSA has not yet hit the highs of previous interest rate hike cycles

- The extent of the hikes off the base of 3.5% has been similar to previous hiking cycles

- Pre-Covid the repo rate hovered around a neutral position of about 6%-7% when inflation was averaging about 4.5%.

- The black line shows forecast 3M JIBAR interest rates implied in the prevailing yield curve. They do not currently suggest a significant cutting cycle

- A cutting cycle would be limited to about 1% currently.

- The risk remains for domestic interest rates to be higher based on domestic fiscal weakness and global EM risks

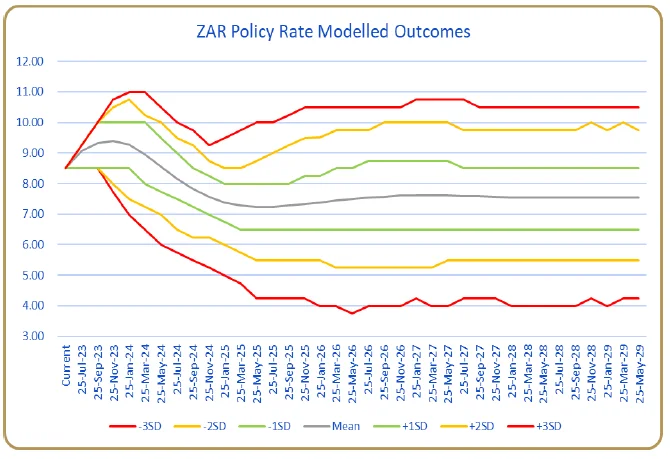

Potential future range of REPO rate

- Bastion regularly performs a mathematical scenario analysis to establish the future potential range of domestic Repo rate trajectories .

- This analysis requires the historic actions of the SARB MPC meetings to be analysed and applied into the future . We run 10 ,000 scenarios to achieve a potential range of interest rates .

- The most useful analysis is the yellow lines which indicate a range of the potential future interest rates within two standard deviations of the mean . The output indicates that with 95 % certainty interest rates will be within the range reflected .

- Our current analysis mathematically indicates that : Based on past interest rate hiking cycles, future Repo rates of 9 -10 % can only be ignored with 5 % certainty

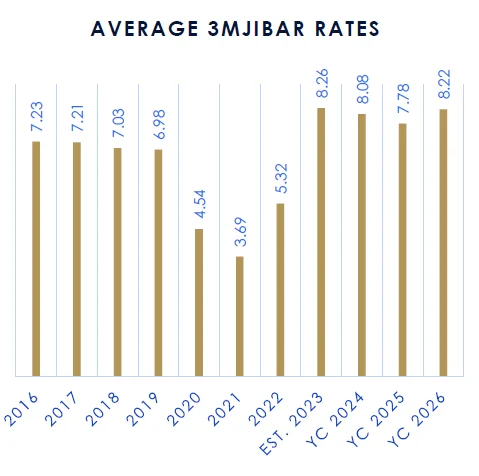

Average Annual 3M JIBAR Analysis – Historical vs. Yield Curve Forecast

- To further analyse the current interest rate cycle it is valuable to look at average annual interest rates historically and those that are currently implied in the prevailing yield curve

- 3M JIBAR averaged approximately 7% per annum for the 5 years leading up to Covid. This dropped to 3.5% as part of the response to the pandemic

- 3M JIBAR is expected to average 8.26% in 2023

- The prevailing yield curve is predicting 3M JIBAR to average as follows:

- 2024: 8.08%

- 2025: 7.78%

- 2026: 8.22%

- By entering into any interest rate hedges currently the company would be locking into these average JIBAR rates for the next few years.

- This requires no premium over the current 3M JIBAR rate of 8.37% nacq.

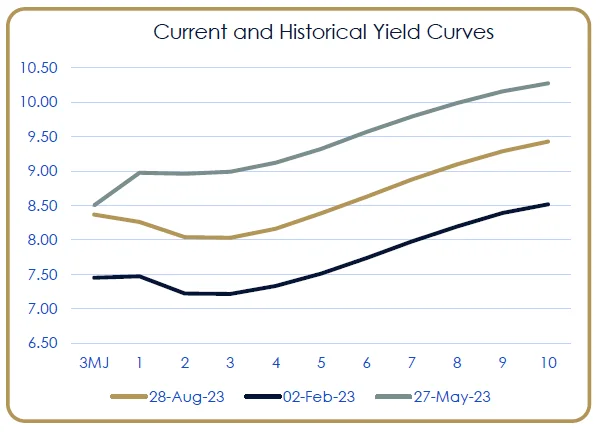

Interest Rate Hedging – Yield Curve analysis

- The copper-coloured yield curve represents the current swap curve and demonstrates that the bearish rate outlook has moderated in the 1-3 year area of the yield curve.

- The yield curve determines where 3M JIBAR can be hedged currently.

- The yield curve has moderated extensively since May 2023.

- RSA has had three rate hikes since Feb 23 which is represented in the difference in the black and copper-coloured curves.

- The increasing longer dated rates in the swap curves reflects the longer term pull of the longer date to RSA bond yields.

- Therefore, Interest Rate Hedging can make sense in the 2-4 year area of the curve.

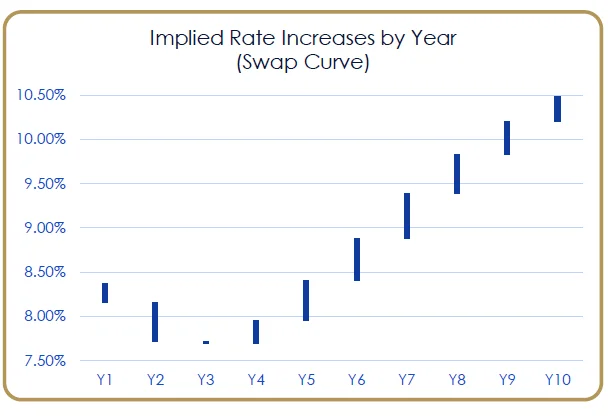

Yield Curve expressed as rate changes per annum:

- The previous slide illustrates the standard way that a yield curve reflects rates and the average rate committed to over a period

- The adjacent chart breaks down the current interest rate yield curve on the previous page into the implied annual interest rates

- This reflects the annual interest rate moves that are baked into the current RSA swap yield curve

- 3M JIBAR benchmark rate is now 8.37%

- The yield curve predicts that there could be a small rate cut in 12 months and a further 50bps rate cut in 12-24 months’ time

- After that we revert to a hiking cycle again

What this means for Interest Rate Hedging Decisions:

- The table reflects indicative mid-market fixed swap rates for interest rate hedges against floating 3M JIBAR.

- The fixed rates offered out to a 4-year duration are trading marginally below current 3M JIBAR before any swap transaction costs.

- Clients may expect a premium over these fixed rates for an ‘all-in’ price. Bastion remains available to assist clients in these negotiations.

- Due to the fixed rates currently trading slightly below 3M JIBAR, entering into a 2 or 3 year interest rate swap is currently very cost effective and would help de-risk a corporate from interest rate hikes until late 2025.

Foreign Exchange Risk – USD/ZAR

The USD/ZAR exchange rate and the crosses are notoriously difficult to forecast. The factors that have the greatest impact on the ZAR exchange rate can be summarised as follows:

- RSA Fiscal Risks (RSA Net Debt/GDP) – continual bail outs, budget deficits while net growth @1%. Rating downgrades;

- RSA Terms of Trade (Nett Exporter vs. Nett Importer) – commodity prices depressed, so nett importer currently;

- RSA Monetary Policy – Interest rate differentials need to remain attractive vs. the major currencies

- Risk ‘on’ vs Risk ‘off’. The global mandate for emerging markets is currently in a Risk ‘off’ phase with concerns over China being the largest EM economy. A trading view on this risk is often expressed by global traders in the ZAR exchange rate.

Many economists currently maintain that using their ‘fair value’ calculators for the ZAR that it is currently under-valued.

In the next slides we analyse what the future trajectory of the ZAR exchange rate may follow and consider whether as an importer the cost of hedging is reasonable or not.

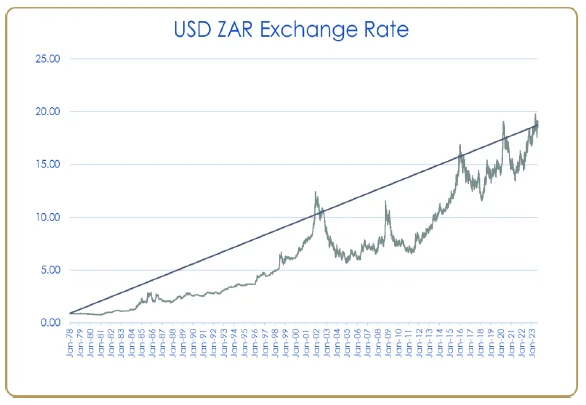

Historical Performance of the ZAR

- The ZAR has depreciated against the USD by approximately 7% per annum since 1978

- This is reflected in the trend line in the adjacent graph

- The overall weakening bias is locked in, however, there are phases when the currency strengthens, as reflected

- For any potential strengthening of the local currency, we would need to see an improvement in some, or all, of the factors mentioned on previous slide

- Over and above this, global interest rates would need to begin reducing making ZAR rates more attractive. There appears little appetite for global interest rates to begin reducing significantly in the next 12M months:

- US Fed Funds Rate

- Current 5.35%

- In 6 months 5.42%

- In 12 months 4.87%

- In 24 months 3.88%

- US Fed Funds Rate

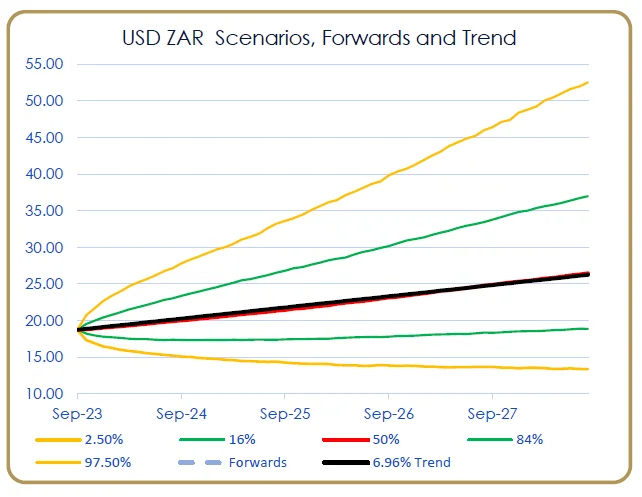

The potential range of USD/ZAR FX rates

- The volatility of the local currency is highlighted strongly in these wide ranges of potential future rates

- The adjacent graph is generated by using Bastion’s Monte-Carlo simulation model to create a range of future foreign exchange rates.

- The yellow lines give a range of potential FX rates to the 2nd standard deviation (95% certainty level).

- The green lines give a range of potential FX rates to the 1st standard deviation (68% certainty level).

- The trend line in the adjacent graph reflects expected future trajectory.

- The output clearly reflects that the risk of a worse exchange rate is higher than an improvement based on current trajectory.

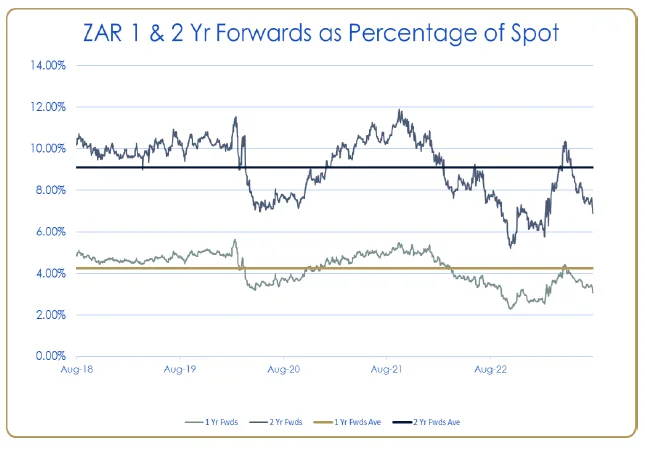

Cost of Currency Hedging Currently:

- The need to hedge foreign exchange depends on the risk to the company or project on a materiality basis.

- As an importer FX hedging can be optimised when the forward points, i.e., the cost to hedge is as low as possible.

- We have compared the cost of hedging forward in the 1-2 year area over the past 5 years in the adjacent graph.

- The output shows that current FX hedging costs are below the 5-year averages.

- Clients who wish to hedge foreign exchange risk can currently take advantage of the reduced cost to hedge. Bastion is able to assist clients in this regard.